A common question from California Veterans when applying for a VA loan is “What is the VA Funding Fee?” The VA mortgage program has many benefits, including no down payment and no monthly mortgage insurance. There is one unique cost however, that is known as the VA Funding fee. The funds from this fee go directly to the VA to help cover potential losses on mortgages that default. The VA Funding Fee is based on a percentage of the loan amount that is dictated by the type of military service that the Veteran performed. Other factors that play a role in the size of your Funding Fee include whether you are paying a down payment or are a first time VA borrower. When it comes to paying the VA Funding Fee, the borrower has the option to either include the VA Funding Fee as part of the loan amount or to pay it in cash upon loan closing.

Example of First Time Use VA Funding Fee

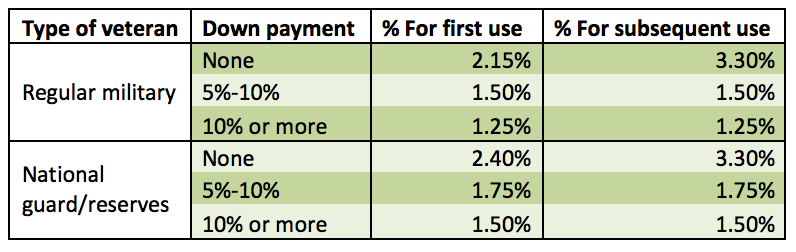

In most cases the Veteran will choose to finance the VA funding Fee into the loan. For example, using the chart below, let’s assume a Regular Military Veteran is purchasing a $400,000 California home with $0 down payment and will be using the VA Home Loan benefit for the first time. The VA Funding Fee will be 2.15%. To calculate the VA Funding Fee, we multiply $400,000 x 2.15% to get $8,600. If the Veteran chooses to finance the Funding Fee, then the total VA loan will be $408,600. **(In 28 years of closing VA loans I do not remember a case where a Veteran chose to pay the VA Funding Fee out of pocket. But it’s possible.) **

Example of Subsequent Use VA Funding Fee

If a California Veteran uses VA financing at a later time, whether to purchase a different home or to do a VA cashout refinance, he would then be subject to a 3.3% VA Funding Fee if the down payment is less than 5%. Assuming the same $400,000 purchase price, but this time for a Veteran who had used VA financing previously, the VA Funding Fee would be $13,200 and the total VA loan would be $413,200. If the Veteran had the ability to put even just 5% down to make the base loan $380,000, the VA Funding Fee would only be 1.5% $5,700. So a “move up” buyer could save on the VA Funding Fee by putting at least 5% down.

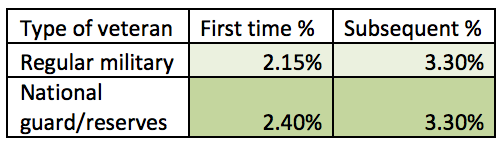

It’s important to note that when refinancing to pull cash out, the VA Funding Fee will either be 2.15% for First Time Use(2.4% for National Guard or Reserves), or 3.3% for subsequent use. The loan to value of the refinance will not help or hurt the Funding Fee calculation.

This chart below lays out what the funding fee will amount to on a VA purchase loan:

This following chart shows you the funding fee percentage for VA cash-out refinances:

Can the VA Funding Fee be Waived?

For those Veterans with a service connected disability and disability rating issued by VA, the Funding Fee will be waived. Whether the rating is 10% or 100%, the Funding Fee will be $0. The VA Certificate of Eligibility will verify for the lender whether a Funding Fee will be required.

Authored by Tim Storm, an Orange County VA Loan Officer specializing in VA Loan. MLO 223456. – Please contact my office at the Home Point Financial. My direct line is 949-640-3102. www.CaliforniaVALoanExpert.com. I will prepare custom VA loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

Having Zero Entitlement on your Certificate of Eligibility doesn’t mean you can’t buy home with Zero down payment using a VA loan. Earlier this year, an Air Force Veteran and his wife were considering the purchase of a new home. Being experienced homeowners, they began the mortgage pre-qualification process with a local mortgage professional. At the conclusion of the pre-qualification process, the mortgage professional determined that they were not eligible for a VA loan. The basis for the conclusion was that the Certificate of Eligibility (COE) showed the Veteran had ZERO entitlement available. Eventually they were offered an FHA home loan to buy the house and they successfully bought the home they had fallen in love with. But, that’s not the end of the story. (Read about VA Entitlement Codes.)

In order to close escrow and successfully purchase this home using an FHA loan, they were required to come up with a down payment of 3.5%, which they had not been expecting. Additionally, they were required to come up with pay the FHA Up Front Mortgage Insurance Premium (UFMIP) of more than $6,200. To put a little more salt in the financial wound, they were also required to pay a monthly Mortgage Insurance Premium (MIP) of $255. And, in case you weren’t aware, FHA MIP never goes away on its own. There are only a few ways to get rid of that monthly expense, including a refinance out of the FHA loan into either a VA loan at any LTV, or some other type of loan at 80% LTV or less.

Not All Mortgage Professionals Are Created Equal

A few months after the couple moved into their new home, they wondered if they could have used a VA loan to buy the home. They searched the internet for a California VA loan specialist who they could call to discuss their situation. After only a brief conversation and a few pointed questions, we determined they most likely could use a VA loan to finance their home. Additional good news was that it wasn’t too late to save a lot of money. The difference between the response they got before and the results we came up with together, have to do with something called Bonus Entitlement. Most Loan Officers do not understand how Bonus Entitlement works, or that it even exists. This is one of the reasons why Veterans should always work with a Loan Officer who lives and breathes VA loans.

Bonus Entitlement – What is it?

Before discussing Bonus Entitlement, it’s important to clearly understand the VA Guaranty. The VA guarantees the mortgage lender up to 25% of the loan amount, in the event the buyer defaults on the loan. This VA Guaranty is called the Veteran’s Basic Entitlement, and it amounts to $36,000. So if you’re buying a home that costs no more than $144,000, you can buy the home with no down payment. That’s right, the math is pretty simple: $144,000 / 4 = $36,000.

While that may be great news in some parts of the U.S., it doesn’t get Veteran’s into homes in most of California. This is where Bonus Entitlement comes in. This is also where the other mortgage professional let our Veteran down. The fact of the matter is that Eligible Veterans have a combined entitlement of Basic + Bonus, which can be used together to finance a home.

Your Bonus Entitlement is calculated in the same way your Basic Entitlement is calculated. However, instead of using the Basic purchase price of $144,000, we use the maximum VA Loan Limits by County in which you intend to live. In the case of our clients above, they were buying in a county where the limit was $636,150.

And again, using the same math to derive the Basic Entitlement, we see the following: $679,650 / 4 = $169,912.

Before we can calculate the correct Combined Entitlement for our clients, we need to keep in mind that the COE showed they had ZERO Basic Entitlement remaining. So their combined entitlement would be calculated by reducing their Bonus Entitlement by the amount of their Basic Entitlement previously used and not restored, as follows:

Bonus Entitlement: $169,912

Less Basic Entitlement: $36,000

Combined Entitlement $133,912

Now it’s time to remember the VA Guaranty, that says they’ll cover 25% of the Loan Amount. That means that we now know the maximum Loan Amount for our clients to finance a home with a VA loan using no down payment or equity. All we have to do is take the Combined Entitlement and multiply it by 4, giving us the maximum loan amount for this particular county for our Veteran of $535,650. Once we knew the current loan amount was only $360,000, we were able to confidently lock in a significantly lower interest rate than their FHA loan. Additionally, we removed the monthly Mortgage Insurance with their new VA loan. Even better, the COE showed the Veteran was disabled and was to required to pay ZERO Funding Fee.

In the end, it worked out for this couple. But the difference between an experienced Mortgage Professional and an experienced VA Mortgage Professional, can sometimes make or break your deal. And even though this couple got their home, they paid thousands of dollars needlessly and had to go find a true VA loan Expert to help them get the loan they deserved.

Authored by Tim Storm, a California Loan Officer specializing in VA Loans. MLO 223456. – Please contact my office at the Home Point Financial. My direct line is 949-640-3102. www.CaliforniaVALoanExpert.com. I will prepare custom VA loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

When it comes to financing a home in California, the options seem nearly endless. Even homeowners who’ve been through the process many times will tell you that it can be a challenging just trying to choose a lender. And each lender you speak with will have their own recommendations for what’s best for you. Because of this, many California Veterans who are perfectly eligible for a VA Loan, will frequently choose a non-VA loan. After spending more than 25 years helping Veterans finance their homes here in California, I can tell you that the most common reason for a Veteran choosing a non-VA loan product, is because the loan officer they worked with either didn’t know enough about the benefits or they simply didn’t offer it.

To be sure, many Veterans don’t understand the program well enough, or they may have been told that the process of obtaining a VA loan is too complicated or too expensive. If you are a Veteran who’s about to enter into the process of financing a home, the very best thing you can do is to get informed about how the VA Loan Program works. You need to become your own expert advisor. And if you want to avoid getting bogged down in the minutiae of program details, you might start with a more “bite-sized” approach like the Top Ten VA Loan Benefits for a California Veteran.

Let’s take a little bit of time to understand the primary benefits of using the VA Loan.

Zero Down Payment

Most people have to save for many years to come up with a sufficient down payment necessary to buy their first home. That’s not the case for eligible Veterans or their surviving spouses. In most cases, this is absolutely the biggest benefit to the program. Even an FHA loan requires a minimum 3.5% down payment. On a $500,000 purchase, that’s $17,500. So if you haven’t yet saved up that kind of money, financing 100% of the purchase price could make a lot of sense.

No Monthly Mortgage Insurance

You’re likely familiar with the term “skin in the game”. In the case of a Zero Down Payment loan, the homebuyer has no skin in the game. Statistically, when homeowner’s buy a home without putting any of their hard-earned savings into buying the property, they are more likely to walk away when unexpected events affect their household income. So Lenders impose something called Mortgage Insurance to offset the risk of that happening. Or at least, non-VA lenders do.

For example: Let’s say you’re buying a $500,000 home using an FHA loan with 3.5% down and 96.5% Loan to Value (LTV). You’d need to pay more than $300/month in addition to your mortgage payment. However, if you used your VA eligibility and financed 100% of that $500,000 purchase price, you would pay no Mortgage Insurance at all. That’s another Zero for you.

Lower Rates than Conforming Loans

Not all 30 Year Fixed Rate Mortgages are created equal. As you begin your search for a suitable lender, you’ll begin to notice a difference in the interest rate lenders offer. Whether you’re looking at a Conventional Conforming, an FHA Conforming, or a VA Conforming 30 Year Fixed Rate mortgage, they all come with essentially the same terms; fully amortized with a fixed rate for the entire 30 years. However, one of the key differences is the rate offered on each.

Using our hypothetical $500,000 loan amount, a 0.25% discount to the rate works out to a little over $70 per month. That may not sound like much, but after a year, you save over $800. And after 30 years of making monthly payments on the loan, you would have saved approximately $26,000 in Interest. The choice is yours, you can either pay the bank that money, or use the VA Loan with a lower interest rate and save the expense altogether.

Multiple Purposes

In the mortgage business, there are only 3 different types of transactions. Every time you finance a home, you will be engaged in one of these three types. You’re either buying a home, refinancing a current mortgage to improve your rate & terms, or you’re refinancing to take cash out of the equity in your home; a Purchase Transaction, a Rate & Term Refinance, or a Cash Out Refinance respectively. Unlike some other loan products (like the CalVet loan which can’t be used for refinancing), the VA Home Loan can be used for either of these transaction types.

The Purchase Transaction is pretty straightforward and is of course used for the purchase of a home using VA financing.

There are two types of VA refinance programs. Let’s look at the VA Cash Out Refinance. If your current mortgage is either a Conventional Conforming, or an FHA loan, you can use your VA Benefits to refinance your mortgage debt into a VA Loan. Many Veterans will use this approach to pay off non-VA loans, which often have costly Mortgage Insurance included into their monthly payments. In this situation, you might lower both the rate and the monthly payment AND get rid of your Mortgage Insurance at the same time. Even if you are not receiving cash “in hand” at the closing, VA considers the refinance of a non-VA loan into a VA to be “cash out”. If your home has appreciated in value since you bought it, you’ll have created Equity – skin in the game – in your home ownership. You can turn that equity into cash by refinancing with a VA Loan. This VA Cash Out Refinance is available to all eligible Veterans, even if your current loan is not a VA Loan. With this type of transaction, your home is now worth more than your current loan balance and you can use the VA Loan to borrower up to 100% of the value of the home, At the close of escrow, you will be issued the cash, which you can use for any purpose you choose. So if you have other debts at a higher interest rate, or you’re looking to make some home improvements, this option could be available to you.

And finally, no discussion of VA Refinance deals can be complete without talking about the Interest Rate Reduction Refinance Loan – “IRRRL“ (pronounced Earl). This is a Rate and Term Refinance since there is not cash out allowed. This is used when you’re refinancing an existing VA Loan in order to improve either your rate or your terms – or both. Remember when we said earlier that the mortgage process can be challenging for even the experienced home owners? Well, the IRRRL simplifies everything for eligible Veterans. In a normal mortgage transaction, applicants are required to provide their lender complete tax returns for at least 2 years, all W-2 Earning Statements for the previous 2 years, Paycheck stubs from the past 30 days, complete bank statements for the previous 2 months and a full appraisal. And that’s just to get your application in front of an underwriter. With an IRRRL, all of that goes away. It streamlines the process for Eligible Veterans, giving you a faster, less expensive and relatively stress-free option to improve the rate & terms of your mortgage debt. Read up on other facts about the IRRRL program here.

Good for Condos

Some of the most affordable housing options for first time home buyers are condominiums. Both from a size and practicality standpoint, buying a condo when you’re young, gets you into the housing market. In many cities, a Condo might be your only affordable option. Unfortunately, many Realtors and lenders feel that financing a Condo with a VA Loan is either too difficult or can’t be done at all. One reason for this is that condominium projects must be approved by the VA before they can be financed with a VA Loan.

For all of these reasons, it’s important to work with a lender who is familiar with VA Approved condominium projects in your area. The VA keeps a list of all VA Approved Condo projects and that list is updated regularly. As a consumer, you (and your lender) have the ability to access this list and discover whether or not the Condo project you’re looking at is VA Approved. You can find that search engine here. All you need is the name of the project, the City, State & County, and you’ll be able to avoid a lot of unnecessary gridlock later on. You can even use this tool to find how many projects in your city are already approved by the VA. A California VA loan specialist can help with determining whether a condo project is VA approved. In Orange County there is a great website listing VA approved condos for sale.

Surviving Spouses May Be Eligible

If you are the surviving husband or wife of a Service member who was killed in action, and you have not yet remarried, you can buy a new home with Zero Down Payment and no Mortgage Insurance using your fallen spouse’s benefits. Additionally, under these circumstances, your VA Funding Fee would also be waived. We’ll discuss the Funding Fee in more detail later. The VA Loan benefit was created to honor the debt of service our country owes Veterans. And although there’s no way to ever repay the debt paid by our fallen Service members, the program allows Surviving Spouses the opportunity to move forward after their loss. You can find more information about benefits for Surviving Spouses on the VA website.

More Lenient Credit Guidelines

As our country continues to emerge from the “greatest recession since the Great Depression”, consumers all across the country are rebuilding their credit. Whether dealing with something as devastating as a Bankruptcy or a mortgage Foreclosure, or far more common like the overall Credit Score or a few late payments, VA Credit guidelines are among the most lenient in the mortgage industry. So when you go comparing lenders and the loan options they offer, a VA Loan makes it easier for eligible Veterans to get into a home loan.

Perhaps the best example of this can be demonstrated with Foreclosures. Consumers who have foreclosed on a property in the past, must wait 7 years before they can become eligible for Conventional Conforming financing. FHA guidelines require a 3 year waiting period, which is significantly better. However, the VA feels that Veterans need only wait 2 years before applying for a VA loan after foreclosure. Generally speaking, eligible Veterans who have experienced either moderate or significant credit challenges in the past, will have an easier time qualifying for a VA Loan. Again, the goal is to make home ownership accessible to eligible Veterans, and the VA Loan does exactly that.

Potential Funding Fee Waiver

In order to offset the costs associated to offering the VA Home Loan program to eligible Veterans, the VA charges something called the VA Funding Fee. Depending on several variables, this Funding Fee can be as little as .50% or as much as 3.3% of the loan amount. While that may sound expensive, it’s important to keep in mind the objectives of the VA Home Loan program; to get more Veterans into homes without requiring a lot of money “out of pocket”. In other words, in most cases, this funding fee can be wrapped into the mortgage loan amount.

Some Veterans will not need to pay for the Funding Fee at all. If you are a disabled Veteran and part of your compensation is the result of a service connected disability, you may be exempt from the Funding Fee. A quick review of the Certificate of Eligibility will determine whether you are eligible for the Funding Fee Waiver. And one last point on the Funding Fee Waiver: Waivers can be given to more than just the Disabled Veteran. Spouses and Surviving Spouses of Deceased Veterans are also covered.

Limit on Closing Costs

Since the VA Home Loan program involves a Veteran’s benefit, VA policy has evolved around the objective of helping Veterans use their benefit to buy a home when they might not otherwise qualify. In light of that goal, the VA limits the amount of fees that can be charged a Veteran to obtain a loan. More restrictive limits cannot be found with other types of loans.

One example of this is the Lender’s Fee. Unlike other loan products, the VA limits the amount a Lender can charge the Veteran to a flat rate of 1%. Additionally, there’s a list of Prohibited Fees, including Attorney’s Fees, Brokerage Fees, Inspection Fees and even some fees associated to appraisals In a Conventional Loan, these fees can add up to thousands of unexpected dollars, but are prohibited under VA guidelines.

Reusable Benefits That NEVER Expire

Many Veterans believe that they can only use their VA Loan benefits once. However, the truth is far better. You can use your VA loan eligibility multiple times. many Veterans buy their first home when they are young and often single. And as their immediate family grows, so too do their needs for living space. When your family outgrows your current home, it begins to make sense to sell it and then buy a larger home that is better suited to meet your family’s needs. After you sell your home and pay off your original VA Loan completely, your VA Benefit entitlement is restored and you can use it again to buy another home. Even if you keep your home, Veterans can also receive a one-time restoration of benefits after they pay off their existing VA Loan. Even if you keep the home after refinancing into a Conventional loan, you can still receive this benefit restoration.

Saving the best for last, it’s crucial to know that your benefits Never Expire. So whether you served 10 years ago or 50 years ago, your VA Home Loan benefits never go away. The first step in home buying process is to retrieve your Certificate of Eligibility. The easiest way to do this is to have your California VA loan specialist retrieve your Certificate of Eligibility for you. You are also able to do it on your own by going to the the VA Benefits Gateway website and request a copy of your Certificate of Eligibility.

There are a lot of other real benefits available to eligible Veterans with the VA Home Loan program. And whether you’re a First Time Home Buyer, or a seasoned veteran of home ownership, the California VA Home Loan program may be right for you. Get informed about your eligibility, become your own best expert, and work with a Lender who is an expert in VA Home Loan financing in California.

Thank you for your service to our country.

Authored by Tim Storm, a California Loan Officer specializing in VA home Loans. MLO 223456. – Please contact my office at the Home Point Financial. My direct line is 949-640-3102. I will prepare custom VA loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

There is more than one type of VA refinance program available for California Veterans. While the most common type of VA refinance program is the VA Interest Rate Reduction Reduction Refinance, or VA IRRRL, the VA cashout refinance is also very a very popular VA refinance program.

What is a VA IRRRL?

A VA Interest Rate Reduction Refinance, also know as an IRRRL or VA Streamline Refinance, is only for current VA borrowers.You must already be in a VA loan. It offers a great benefit to current VA loan borrowers because it allows for an easy way to take advantage of improving interest rates.

The Veteran must already have a VA loan

No cash out is allowed. This program is strictly a “Rate and Term” refinance.

No income documentation is needed. Employment is verified, but debt to income ratios are not reviewed.

No asset verification, meaning no bank statements needed, unless the Veteran will need money to close the IRRRL.

No appraisal or termite report required. This is the best part and makes the time to close a VA IRRRL very short since the lender doesn’t have to wait for an appraisal or termite inspection report.

The Veteran must either be lowering their interest rate and payment, shortening the term (some qualifying requirements may be needed if the payment is going up), or going from an Adjustable Rate Mortgage to a Fixed rate.

The VA IRRRL is so easy to close that it is also advertised heavily by some lenders who don’t always have the Veterans best interest in mind. Current VA borrowers are used to receiving mailers from lenders offering interest rates that are “too good to be true” (in the words of many of my clients). Make sure to read the fine print, or contact a VA lender you trust for advice on whether a VA IRRRL makes sense for you. Also, while some lenders will advertise that you will “skip payments”, that is never the case with any type of refinance. Mortgage interest will be collected and paid on the loan being paid off every time. It’s just a matter of whether you choose to have it added to the new loan or pay it out of pocket. Make sure you know how much you will save monthly, as well as what the “breakeven” time period will be on your refinance. Make sure you will breakeven prior to when you think you will sell your home.

Any VA refinance that is not an IRRRL is a “cash out refinance”. Even if the Veteran will not be receiving cash out at closing, VA still considers the refinance to be “cash out” if the borrower is refinancing from a non-VA loan. And why, you ask, would someone choose to refinance from a non-VA loan into a VA loan. There are many reason, including:

VA interest rates tend to be lower than most other types of loan programs. And the interest rate spread widens in favor of VA for borrowers whose FICO scores are lower than 740, or are pulling cash out, or have a loan to value of 80% or higher.

Some lenders will allow VA refinancing for borrowers with FICO scores as low as 580. That can’t be done with Conventional financing.

VA allows “cash out” refinancing up to 100% of the property value. Conventional programs cap out at 80% of the value. Also, unlike Conventional financing, there are no “pricing adjustments” for the worse for pulling cash out with a VA loan.

VA has much shorter wait periods after major credit events like a bankruptcy (2 years after discharge for VA versus 4 years for Conventional), foreclosure (2 years for VA versus 7 years for Conventional) or short sale.

VA allows for higher debt to income ratios (no cap – not unusual to have debt to income ratios above 50% on a VA loan versus a cap of 45% on Conventional financing)

Jumbo VA program allows for cash out at a much higher loan to value than standard Jumbo programs. For example, in Orange or Los Angeles counties, where the VA loan limit for 100% financing is $636,150, a Veteran could pull cash out to a little over 90% of the property value if the appraisal was in the $1,000,000 range. And it would be at a lower rate than comparable Jumbo programs.

Typical Uses of Cash Out from a VA Refinance

The Veteran can use the cash out for just about any purpose. But the most common purposes are listed below.

Debt Consolidation. This is a great way to pay off high interest rate credit cards that you are carrying the balance on.

Home Improvements. – with property values increasing over the past few years, Veterans now can take advantage of their equity and improve their homes, whether it is paint, flooring, a kitchen remodel, etc. Since the loan can be up to 100% of the property value, it acts as a far easier way to improve your home versus a construction loan.

Refinance from a CalVet Loan. Because CalVet does not refinance, Veterans end up locked into an interest rate that is higher than the market. They aren’t able to do a VA IRRRL because their loan is CalVet, not VA. Refinancing their CalVet loan into a VA loan can lower their payment and give them access to the VA IRRRL if rates drop later.

Education. College is expensive. Many Veterans will take advantage of the VA cashout refinance program to help cover college expenses for their kids.

Pay off a HERO or PACE loan. The HERO loan program is used for energy efficient improvements to the home. It is most typically used for solar panels, but can include other energy efficient improvements as well. In many cases it is then paid through the annual property tax bill. Depending on the size of the HERO loan, the tax bill increase can catch some people off guard. And if they have an impound account for property taxes, it can also throw their lender off guard when the property tax bill comes in much higher than expected, resulting in the lender increasing the monthly mortgage payment to make up for the higher tax bill. Using a VA cash out refinance to payoff the HERO loan will put the property tax payment back down to a reasonable level.

For someone who has never had a VA loan it is important to know that VA does require a few things that are not required with other types of financing. With VA, there will most likely be an impound/escrow account for property taxes and insurance. This means you will pay 1/12 of your property taxes and homeowners insurance each month as part of your mortgage payment. Also, VA requires a clear termite report prior to closing. And the last important thing to know is that VA requires a Funding Fee on cash out refinances (and purchases). Depending on whether you have used VA financing previously, the Funding Fee can be as high as 3.3% of the loan. It can be financed into the loan amount. For Veterans who have a disability, their Certificate of Eligibility will inform the lender to waive the VA Funding Fee.

The best way to determine whether a VA refinance is for you, and what your option are, is to call a California VA loan offer who specializes in the VA loan program. The Loan Officer should be able to provide custom loan scenarios that will not only show the payment breakdown, but also accurately estimate the closing costs and cash going back to you.

Authored by Tim Storm, a California Loan Officer specializing in VA home Loans. MLO 223456. – Please contact my office at the Home Point Financial. My direct line is 949-640-3102. I will prepare custom VA loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

Finding an accurate VA Loan calculator is not an easy task for California Veterans. Researching and doing your due diligence is important when in the process of searching for a VA loan to purchase or refinance a home. Some mortgage websites provide a loan calculator...

Having Zero Entitlement on your Certificate of Eligibility doesn’t mean you can’t buy home with Zero down payment using a VA loan. Earlier this year, an Air Force Veteran and his wife were considering the purchase of a new home. Being experienced homeowners, they began the mortgage pre-qualification process with a local mortgage professional. At the conclusion of the pre-qualification process, the mortgage professional determined that they were not eligible for a VA loan. The basis for the conclusion was that the Certificate of Eligibility (COE) showed the Veteran had ZERO entitlement available. Eventually they were offered an FHA home loan to buy the house and they successfully bought the home they had fallen in love with. But, that’s not the end of the story. (Read about

Having Zero Entitlement on your Certificate of Eligibility doesn’t mean you can’t buy home with Zero down payment using a VA loan. Earlier this year, an Air Force Veteran and his wife were considering the purchase of a new home. Being experienced homeowners, they began the mortgage pre-qualification process with a local mortgage professional. At the conclusion of the pre-qualification process, the mortgage professional determined that they were not eligible for a VA loan. The basis for the conclusion was that the Certificate of Eligibility (COE) showed the Veteran had ZERO entitlement available. Eventually they were offered an FHA home loan to buy the house and they successfully bought the home they had fallen in love with. But, that’s not the end of the story. (Read about

When it comes to financing a home in California, the options seem nearly endless. Even homeowners who’ve been through the process many times will tell you that it can be a challenging just trying to choose a lender. And each lender you speak with will have their own recommendations for what’s best for you. Because of this, many California Veterans who are perfectly eligible for a VA Loan, will frequently choose a non-VA loan. After spending more than 25 years helping Veterans finance their homes here in California, I can tell you that the most common reason for a Veteran choosing a non-VA loan product, is because the loan officer they worked with either didn’t know enough about the benefits or they simply didn’t offer it.

When it comes to financing a home in California, the options seem nearly endless. Even homeowners who’ve been through the process many times will tell you that it can be a challenging just trying to choose a lender. And each lender you speak with will have their own recommendations for what’s best for you. Because of this, many California Veterans who are perfectly eligible for a VA Loan, will frequently choose a non-VA loan. After spending more than 25 years helping Veterans finance their homes here in California, I can tell you that the most common reason for a Veteran choosing a non-VA loan product, is because the loan officer they worked with either didn’t know enough about the benefits or they simply didn’t offer it. begin to notice a difference in the interest rate lenders offer. Whether you’re looking at a Conventional Conforming, an FHA Conforming, or a VA Conforming 30 Year Fixed Rate mortgage, they all come with essentially the same terms; fully amortized with a fixed rate for the entire 30 years. However, one of the key differences is the rate offered on each.

begin to notice a difference in the interest rate lenders offer. Whether you’re looking at a Conventional Conforming, an FHA Conforming, or a VA Conforming 30 Year Fixed Rate mortgage, they all come with essentially the same terms; fully amortized with a fixed rate for the entire 30 years. However, one of the key differences is the rate offered on each.  Perhaps the best example of this can be demonstrated with Foreclosures. Consumers who have foreclosed on a property in the past, must wait 7 years before they can become eligible for Conventional Conforming financing. FHA guidelines require a 3 year waiting period, which is significantly better. However, the VA feels that Veterans need only wait 2 years before applying for a

Perhaps the best example of this can be demonstrated with Foreclosures. Consumers who have foreclosed on a property in the past, must wait 7 years before they can become eligible for Conventional Conforming financing. FHA guidelines require a 3 year waiting period, which is significantly better. However, the VA feels that Veterans need only wait 2 years before applying for a  Since the VA Home Loan program involves a Veteran’s benefit, VA policy has evolved around the objective of helping Veterans use their benefit to buy a home when they might not otherwise qualify. In light of that goal, the VA limits the amount of fees that can be charged a Veteran to obtain a loan. More restrictive limits cannot be found with other types of loans.

Since the VA Home Loan program involves a Veteran’s benefit, VA policy has evolved around the objective of helping Veterans use their benefit to buy a home when they might not otherwise qualify. In light of that goal, the VA limits the amount of fees that can be charged a Veteran to obtain a loan. More restrictive limits cannot be found with other types of loans. There is more than one type of VA refinance program available for California Veterans. While the most common type of VA refinance program is the VA Interest Rate Reduction Reduction Refinance, or

There is more than one type of VA refinance program available for California Veterans. While the most common type of VA refinance program is the VA Interest Rate Reduction Reduction Refinance, or  The VA IRRRL is so easy to close that it is also advertised heavily by some lenders who don’t always have the Veterans best interest in mind. Current VA borrowers are used to receiving mailers from lenders offering interest rates that are “too good to be true” (in the words of many of my clients). Make sure to read the fine print, or contact a VA lender you trust for advice on whether a VA IRRRL makes sense for you. Also, while some lenders will advertise that you will “skip payments”, that is never the case with any type of refinance. Mortgage interest will be collected and paid on the loan being paid off every time. It’s just a matter of whether you choose to have it added to the new loan or pay it out of pocket. Make sure you know how much you will save monthly, as well as what the “breakeven” time period will be on your refinance. Make sure you will breakeven prior to when you think you will sell your home.

The VA IRRRL is so easy to close that it is also advertised heavily by some lenders who don’t always have the Veterans best interest in mind. Current VA borrowers are used to receiving mailers from lenders offering interest rates that are “too good to be true” (in the words of many of my clients). Make sure to read the fine print, or contact a VA lender you trust for advice on whether a VA IRRRL makes sense for you. Also, while some lenders will advertise that you will “skip payments”, that is never the case with any type of refinance. Mortgage interest will be collected and paid on the loan being paid off every time. It’s just a matter of whether you choose to have it added to the new loan or pay it out of pocket. Make sure you know how much you will save monthly, as well as what the “breakeven” time period will be on your refinance. Make sure you will breakeven prior to when you think you will sell your home. Typical Uses of Cash Out from a VA Refinance

Typical Uses of Cash Out from a VA Refinance