A common question from California Veterans when applying for a VA loan is “What is the VA Funding Fee?” The VA mortgage program has many benefits, including no down payment and no monthly mortgage insurance. There is one unique cost however, that is known as the VA Funding fee. The funds from this fee go directly to the VA to help cover potential losses on mortgages that default. The VA Funding Fee is based on a percentage of the loan amount that is dictated by the type of military service that the Veteran performed. Other factors that play a role in the size of your Funding Fee include whether you are paying a down payment or are a first time VA borrower. When it comes to paying the VA Funding Fee, the borrower has the option to either include the VA Funding Fee as part of the loan amount or to pay it in cash upon loan closing.

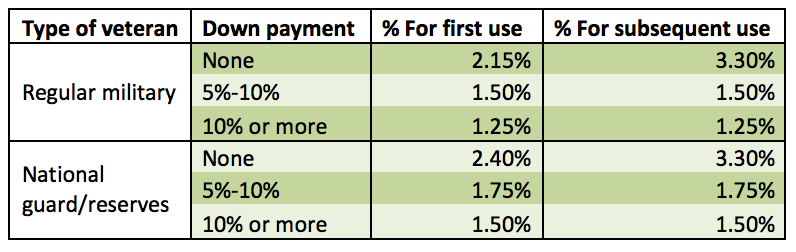

Example of First Time Use VA Funding Fee

In most cases the Veteran will choose to finance the VA funding Fee into the loan. For example, using the chart below, let’s assume a Regular Military Veteran is purchasing a $400,000 California home with $0 down payment and will be using the VA Home Loan benefit for the first time. The VA Funding Fee will be 2.15%. To calculate the VA Funding Fee, we multiply $400,000 x 2.15% to get $8,600. If the Veteran chooses to finance the Funding Fee, then the total VA loan will be $408,600. **(In 28 years of closing VA loans I do not remember a case where a Veteran chose to pay the VA Funding Fee out of pocket. But it’s possible.) **

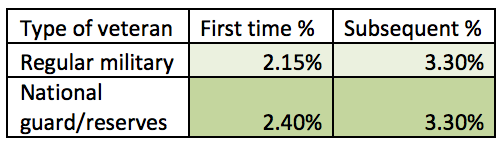

Example of Subsequent Use VA Funding Fee

If a California Veteran uses VA financing at a later time, whether to purchase a different home or to do a VA cashout refinance, he would then be subject to a 3.3% VA Funding Fee if the down payment is less than 5%. Assuming the same $400,000 purchase price, but this time for a Veteran who had used VA financing previously, the VA Funding Fee would be $13,200 and the total VA loan would be $413,200. If the Veteran had the ability to put even just 5% down to make the base loan $380,000, the VA Funding Fee would only be 1.5% $5,700. So a “move up” buyer could save on the VA Funding Fee by putting at least 5% down.

It’s important to note that when refinancing to pull cash out, the VA Funding Fee will either be 2.15% for First Time Use(2.4% for National Guard or Reserves), or 3.3% for subsequent use. The loan to value of the refinance will not help or hurt the Funding Fee calculation.

This chart below lays out what the funding fee will amount to on a VA purchase loan:

This following chart shows you the funding fee percentage for VA cash-out refinances:

Can the VA Funding Fee be Waived?

For those Veterans with a service connected disability and disability rating issued by VA, the Funding Fee will be waived. Whether the rating is 10% or 100%, the Funding Fee will be $0. The VA Certificate of Eligibility will verify for the lender whether a Funding Fee will be required.

Authored by Tim Storm, an Orange County VA Loan Officer specializing in VA Loan. MLO 223456. – Please contact my office at the Home Point Financial. My direct line is 949-640-3102. www.CaliforniaVALoanExpert.com. I will prepare custom VA loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

The VA mortgage program is an excellent option for California’s Veterans when it comes to refinancing home to pull cash out. Similar to how VA allows for 100% financing on a home purchase, VA also allows 100% financing on cash out refinances.

There are two main types of refinance programs available using VA financing. The VA IRRRL or Interest Rate Reduction Refinance Loan, which is also known as a VA Streamline Refinance, is an extremely simplified process that doesn’t require a new appraisal and only needs a minimal amount of documentation. With a streamline refinance, a veteran has the ability to lower their interest rate and/or take time off of their loan term. The VA IRRRL is strictly a “VA to VA” refinance, meaning you must already have a VA loan to take advantage of the IRRRL program. Also, a VA IRRRL DOES NOT ALLOW CASH OUT. And this is where the other VA refinancing program comes into play. A VA cash out refinance is a much more thorough process but allows cash out up to 100% of the property value.

9 Things to Know about a VA Cashout Refinance

The current loan being refinanced does not need to be a VA loan. Yes, you can refinance an FHA or Conventional loan into a VA loan. Many Veterans refinance their CalVet loans into a VA loan since CalVet does not offer refinancing.

VA allows for cashout refinancing up to 100% of the property value. No other program even comes close.

Unlike the IRRRL program, a VA cashout refinance is a fully qualifying loan. Full income and asset documentation, appraisal, and clear termite report are required.

It only takes 30 days to close.

VA interest rates tend to be very competitive with other loan programs, despite the fact that VA will allow 100% financing.

There is no PMI, or monthly Mortgage Insurance (like you would have on other loan program that allow financing above 80% loan to value.

There is a VA Funding Fee, except for those Veterans with a disability rating. (VA waives the Funding Fee for Veterans who have a Disability Rating)

In order to get a VA cash out refinance, California Veterans will need to provide the lender their income and employment documentation. The lender will also need to order a new appraisal of the property to verify the property value and establish the maximum loan amount.

While VA cash out refinances are able to be completed up to 100% value of the property, not all lenders follow will do everything VA allows. With many VA cash out refinances, some lenders will limit the maximum cash out amount to 90% of the property value. If you run into a situation where the lender is limiting your cashout to less than 100% of the property value (and you want the higher loan amount), find another California VA lender who can get you the loan amount you want.

When checking into your options for refinancing, it is important to research and give consideration to all available possibilities. A VA refinance is a great option for California Veterans, but the VA Funding Fee can be steep (unless you get the waiver). If you only need cash out to 80% of the property value, then a Conventional loan may be a better option. Have your favorite California VA Loan Specialist prepare a Side by Side comparison of the programs so that you can see your options.

Authored by Tim Storm, a California VA Loan Officer specializing in VA Loan. MLO 223456. – Please contact my office at the Home Point Financial. My direct line is 949-640-3102. www.CaliforniaVALoanExpert.com. I will prepare custom VA loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

Do you qualify for a California VA loan right now? Do you know what it takes to qualify? California has one of the highest concentrations of Veterans throughout the country but many of them don’t even know that they are eligible for the VA loan program or don’t know what is needed to be qualified. It is very important to understand the basics first. What is the Debt to Income ratio and how high can it go? What are the FICO score requirements? What is Residual Income and how does it factor into qualifying for a VA loan? How long after a bankruptcy or foreclosure can you get a VA loan? What are the VA loan limits in your California county?

What is the Debt to Income ratio and how high can it go?

One of the primary calculations that VA lenders will look at when considering a potential borrower for a VA loan is the Debt to Income ratio. The debt to income ratio is a measurement that compares a Veteran’s monthly debt payments to their monthly gross income (before income taxes). The Department of Veterans affairs has set a guideline for VA lenders of 41% for the Debt to Income Ratio. It is still possible for a Veteran to qualify for a VA loan if their debt to income ratio exceeds that 41% mark, but additional scrutiny will be raised during the loan process. Most VA lenders will allow the Debt to Income ratio to be as high as 50%, while some will even go to 60%. If a VA lender tells you your Debt to Income ratio is too high, ask them what it is. Some lenders are more stringent than others.

What are the FICO score requirements?

The Department of Veterans Affairs doesn’t fund loans, but acts as an insurer for qualified lenders. Because of this, credit score requirements will vary from lender to lender. Many lenders have a minimum credit score requirement of 620, and some will approve a loan with an even lower credit score.(down to 580) If one lender won’t approve your loan request, it can be worth researching other lenders to see if you can find one that will approve your loan.

What is Residual Income and how does it factor into qualifying for a VA loan?

The residual income requirement is one of the reasons why the VA mortgage program is so successful. A veteran’s residual income is their remaining monthly income after they have fulfilled all of their current credit obligations. The VA has set different residual income requirements for veterans based on location and their family size. Residual income also has the ability to reduce the relevance of a veteran’s debt to income ratio. If a veteran’s debt to income ratio is above the 41% guideline, they can offset this if their residual income is 20% greater than the VA guideline.

How long after a bankruptcy or foreclosure before you can get a VA loan?

Foreclosures and bankruptcies are major financial events that many borrowers think will prevent them from getting a mortgage. However, with proper handling of these events and a little bit of effort put into credit repair, these hurdles that can be easily overcome. A Veteran can qualify for a VA loan 2 years after a bankruptcy has been discharged and 2 years after a foreclosure. It’s important to understand that applying for credit after a major credit event is the first step in restoring credit. And make sure to not have any late payments or derogatory credit after bankruptcy or foreclosure.

Since home prices vary in different parts of the country and have risen since the beginning of the VA program, the VA has set county loan limits that dictate the maximum loan amount that a veteran can get without needing a down payment. In Orange and Los Angeles County’s, the VA county loan limit is $679,650. It is possible to get a VA loan that is above the county loan limit, which is known as a Jumbo VA loan. With a Jumbo VA loan a down payment equal to 25% of the different between the purchase price and the county loan limit is required.

Authored by Tim Storm, an California VA Loan Officer specializing in VA Loans. MLO 223456. – Please contact my office at the Home Point Financial, NMLS 7706. My direct line is 949-640-3102. www.CaliforniaVALoanExpert.com. I will prepare custom VA loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

In the first year of home ownership, most home buyers will receive a Supplemental Tax bill. For California Veterans who used VA financing and have their taxes paid from their impound account, receiving a Supplemental Tax bill causes confusion. “Shouldn’t the supplemental tax bill be paid from the impound account?”. In many case, the answer is “no”. This is why it is important to understand what the Supplemental Tax is and to be prepared for it.

How Assessed Values and Tax Bills are Calculated

A home owner’s property taxes are based off of the home’s assessed value when it was purchased. In most cases, the assessed value is the actual purchase price of the home, less exemptions. 100% Disabled Veterans can get their assessed value lower by between $126,380 and $189,571 by applying for the Disabled Veterans Exemption. Each year the assessed value can increase by a maximum of 2%. This limitation is in place because of Proposition 13 (this is specific to California only), which passed in 1978. (I just remember that in 1977 I was in middle school and was required to shower after PE, even if we did nothing. In 1978, when Prop 13 passed, the school could no longer require us to shower since there were no longer school provided towels). The standard property tax is 1%, although nearly every county has additional taxes or assessments that bring the tax rate up to between 1.05% to 1.25%. Some areas, typically newer developments, may even have Mello Roos, but I’ll leave Mello Roos for another discussion. Each year, normally in October, the county sends out tax bills. The assessed value is multiplied by the tax rate. The bill is split into a “first half” due November 1 (late after December 10), and “second half” due Feb 1 (late after April 10).

When a home is sold, in most cases (we’ll try to forget about the whole 2008 debacle when property values dropped) the value for the new owner is higher than for the previous owner. This means that the new buyer will have a new tax amount to pay. But since the county will have already sent that years tax bills out there will be a “catching up” bill sent out several months after the purchase. Instead of calling the bill “Supplemental” they should just call it the Catching Up bill. This difference in property values is what spawned supplemental property tax laws.

A Little History on Supplemental Tax Assessments

Supplemental tax assessment laws were originally enacted here in California in 1983 and were intended to increase funding for schools. This law accelerated the effective date of new appraisals made according to Prop 13. Supplemental tax laws require that a new property assessment be completed after a change in property ownership. If the new value is greater than the previous value, then a Supplemental tax bill will be issued. If the new value is less than the old value, then a refund will be issued to the owner.

When is the Supplemental Tax Bill Sent out?

The bill for Supplemental taxes will come separate from the regular property tax bill and usually comes 6 to 9 months after the purchase. Supplemental taxes are primarily paid as a one time lump sum to make up for the difference between the required tax payments. If the change in ownership happens before May 31st, then there will be two supplemental tax bills. It is solely the responsibility of the buyer to make sure that the supplemental taxes are paid. The Supplemental tax bill will typically state something along the lines of “This bill will has not been submitted to your lender for payment”.

How to Estimate your Supplemental Tax Bill

Fortunately, most county tax websites have a Supplemental Tax Bill Estimator. You can use the online calculator to estimate your impending Supplemental Tax Bill. Below are links to a few of southern California county Supplemental Tax calculators.

If you have questions on the VA loan program in California, or would like to see custom VA loan scenarios, make sure to contact me. I’m always available to help.

Authored by Tim Storm, a California VA Loan Officer specializing in the VA Loan program. MLO 223456. – Please contact my office at the Home Point Financial. My direct line is 949-640-3102. www.CaliforniaVALoans.com. I will prepare custom loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

California VA Loan Limits for some high priced counties in California will be $679,650, which is welcome news for those counties where property values continue to rise. The highest Zero Down VA loan limit in California in 2017 was $636,150. An increase of over $40,000 for Zero Down financing is a big jump.

What the VA Loan Limit Increase Means for California Veterans

For a California Veteran purchasing a home for $679,650 in a county like Orange or Los Angeles, this means they will not need a down payment. Because VA does have the Jumbo VA Loan program, it is possible to get a VA loan above the 100% financing limit. If a Veteran purchased a home for $679,650 in 2017, they would have needed a down payment of $10,875 and a VA loan of $668,775. That was really a good deal. But now, even better, they will not need a down payment at all for a $679,650 purchase price. The Veteran can keep the $10,875 in their bank account, or use for paying closing costs.

100% Financing Limit Varies from County to County

The basic 100% VA loan limit will be $453,100 in 2018. The previous limit in 2017 was $424,100. For counties that are not considered “high cost”, such as San Bernardino and Riverside counties, $453,100 will be their limit. Other counties, like San Diego, will have increased limits compared to 2017 ($612,950 in 2017), which will now be $649,750.

VA Loans Above 100% Financing Limit = Jumbo VA Loan

The Jumbo VA loan is any VA loan that is above the 100% financing limit for the county they are in. For example, if a Veteran purchases a home in Riverside County for $473,100, where the 100% Loan Limit is $453,100, they would need a down payment of $5,000. Notice how I did not say they needed a down payment of $20,000. VA only requires a down payment equal to 25% of the difference between the 100% loan limit and the higher purchase price. This would be a Jumbo VA loan. That same loan amount in Orange County, CA would not be a Jumbo loan. A Jumbo VA loan in Orange County (or Los Angeles county) would occur if the purchase price were above $679,650. For example, if the purchase price was $699,650, then a down payment of $5,000 would be required. If the purchase price was $1,079,650, or $400,000 above the loan limit in Orange County, the down payment would be $100,000 (.25 * $400,000 difference = $100,000 down payment). The VA loan would be $979,650.

High Loan Limits will Help VA Loan Refinancing

The higher loan limits will also help Veterans who currently own homes and were looking to refinance to pull cash out. If their loan amount was limited by the 2017 loan limits, then the 2018 VA loan limit will help. VA allows cashout refinancing up to 100% of the property value when the loan amount is within the 100% financing limits.

How to Find Out What a VA Loan Looks to for You

So how do you find out what the numbers will look like for you. The first step is to contact a California VA loan specialist. A California VA Loan Officer is someone who specializes in VA financing. It is important to work with a specialist when learning about the VA loan program because it is different from other types of loan programs. The California VA Loan Officer should be able to prepare accurate custom loan scenarios that will give you a complete breakdown of the numbers, including the full payment (Principal, Interest, Taxes, and Insurance), closing costs, and prepaid expenses. A good Loan Officer should also be able to answer questions on the VA program and provide a custom video of your loan scenarios.

Authored by Tim Storm, a California Loan Officer specializing in VA Loans. MLO 223456. – Please contact my office at the Home Point Financial. My direct line is 949-640-3102. www.CaliforniaVALoanExpert.com. I will prepare custom VA loan scenarios which will be matched up to your financial goals, both long and short term. I also prepare a Video Explanation of the your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process.

Contact Me

Tim Storm

MLO# 223456 Arbor Financial Group Mortgage Advisor 1805 E Garry Ave Santa Ana, CA 92705

Direct: 949-826-1846

$0 Down Home Loans for Veterans

Get Prequalified for a California VA loan today. You will work directly with Tim Storm.

The VA mortgage program is an excellent option for California’s Veterans when it comes to refinancing home to pull cash out. Similar to how VA allows for 100% financing on a home purchase, VA also allows 100% financing on cash out refinances.

The VA mortgage program is an excellent option for California’s Veterans when it comes to refinancing home to pull cash out. Similar to how VA allows for 100% financing on a home purchase, VA also allows 100% financing on cash out refinances.